What is occurring with cryptocurrency lenders? The bear market has taxed every sector of the cryptocurrency economy, but maybe none more than crypto loan businesses. You are already familiar with BlockFi, Celsius Network, and Genesis Global Trading.

There are others, but these once-respected companies have suffered some of the most embarrassing setbacks this year. All of them are secured by loans against digital assets. What was wrong? And can centralised cryptocurrency lenders reclaim market share and confidence?

Crypto lending connects those who have extra crypto and want to make a return on their funds by depositing it on a platform, which then lends those funds to people who wish to borrow crypto and is ready to put it up as collateral and pay interest to obtain a loan.

As stated by Reuters earlier this year, “crypto lending is essentially banking – for the crypto world.” And, as Lisa from “The Simpsons” famously said, comparisons are typically troublesome.

Before the market crash, lending was a major source of revenue for the sector. Celsius accrued over $11 billion in assets on its platform. BlockFi, which recently filed for Chapter 11 bankruptcy protection, had been valued at $3 billion just last year. Genesis, a Wall Street-facing firm owned by CoinDesk’s parent company, Digital Currency Group, had $2.8 billion in active loans at the end of the third quarter of this year.

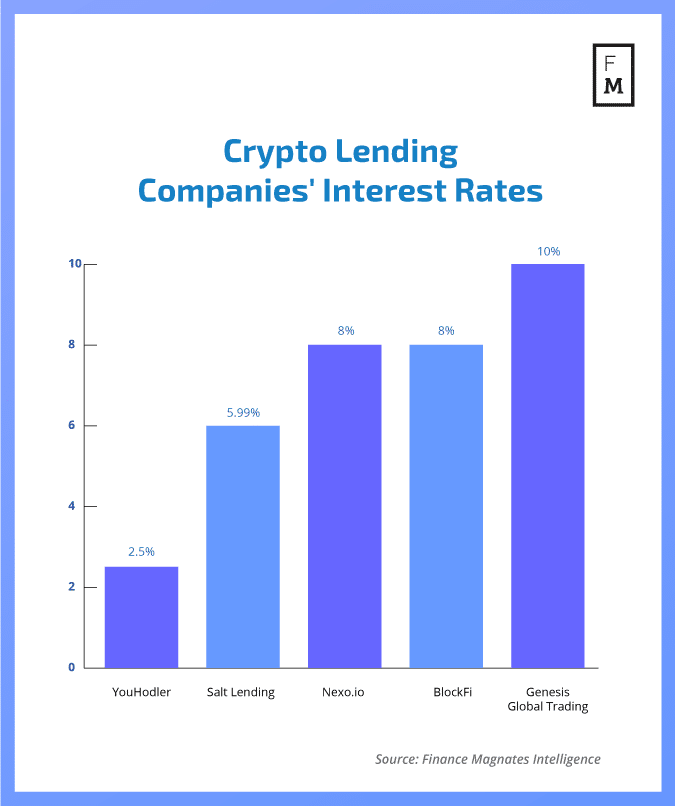

As a result of providing high returns on deposits, crypto lenders grew so huge. A bank account may earn less than 1% in interest, whereas some crypto lenders offer yields of up to 20%. Even at the peak of the bull run, people were puzzled about the source of these returns.

Like banks, crypto lenders were expected to profit by lending out deposits. Borrowers typically pay between 5%-10% in fees, and crypto lenders like Celsius were supposed to profit on the spread between interest payments paid to depositors and fees earned by borrowers.

This year has taught us that the situation can swiftly deteriorate even when things are going well for crypto lenders. Volatility in the markets put pressure on crypto lenders’ normal businesses – including shrinking the number of depositors and borrowers. Faced with an increase in withdrawals, many were discovered to be insolvent or illiquid.

However, some lenders engaged in possibly unlawful activity by re-lending funds they shouldn’t have or making generally unwise wagers. In a filing, Vermont’s securities regulator stated that Celsius occasionally resembled a Ponzi scheme since it relied on luring new investors to pay out existing ones. It accomplished this by establishing reward programs related to its CEL cryptocurrency and using its marketing spend to pay yields well above the norm.

Not all crypto lenders are made equal, nor did these companies fail for the same reasons. Also, there is no reason to believe that other crypto lenders have necessarily exploited client funds. Because these are private enterprises, it is also not quite evident what went wrong.

Increasing calls for cryptocurrency regulation could be beneficial for the industry. Although Federal Deposit Insurance Corporation (FDIC) insurance, which covers up to $250,000 in bank deposits, is unlikely to be granted for crypto lenders, regulatory oversight might be expanded to ensure that these firms manage deposits in a solvent manner.

Notably, the crypto lenders included within the decentralised finance (DeFi) sub-economy performed better. The non-custodial nature of the deposits prevents human actors from seizing them. While crypto lenders can negotiate favourable terms with ostensibly trustworthy individuals, with DeFi everyone follows the same standards.

{kind=link}