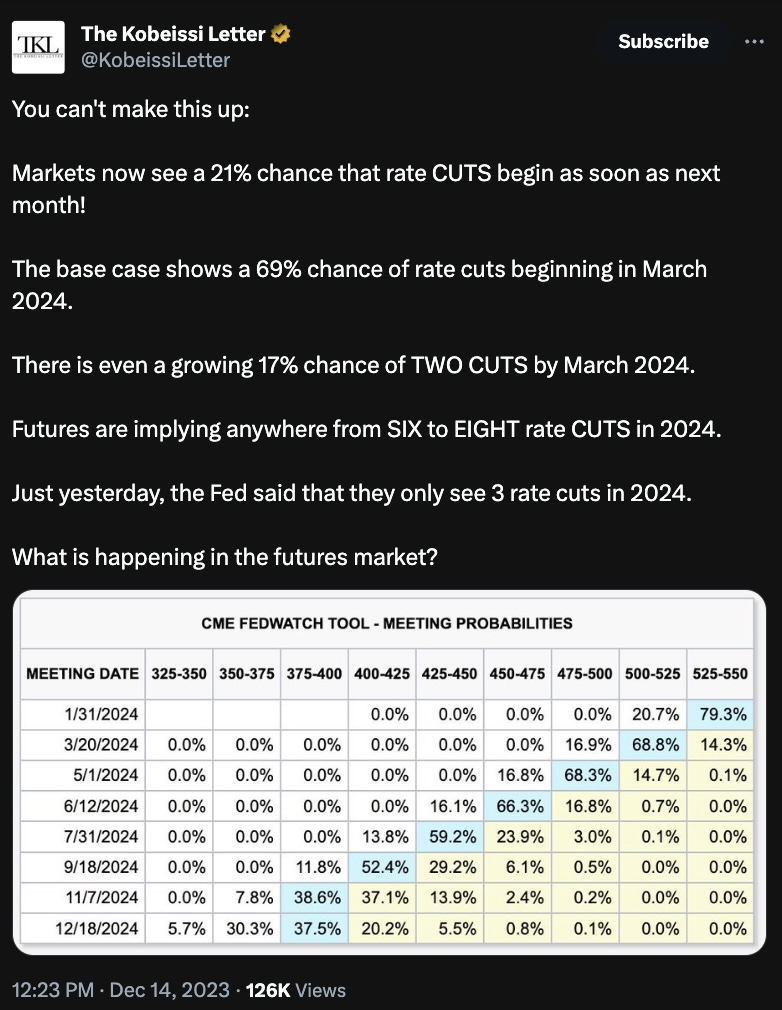

The Federal Open Market Committee’s (FOMC) meeting in December provided a substantial boost to markets, leading risk assets, including cryptocurrencies, to surge as the central bank seemed to adopt a more dovish stance on monetary policy. However, caution is advised as 2024 may bring an unexpected turn, with the Federal Reserve potentially compelled to implement another rate hike to counteract rising prices and meet its 2% inflation target.

Despite prevailing expectations that the Fed has successfully tamed inflation, economic analysis suggests otherwise. The recent deceleration in price growth is likely transient, and inflation is poised to spike to approximately 3.5% by the end of next month, persisting well into 2024. This poses a challenge for the central bank, obligated by its dual mandate to regulate prices while sustaining maximum employment.

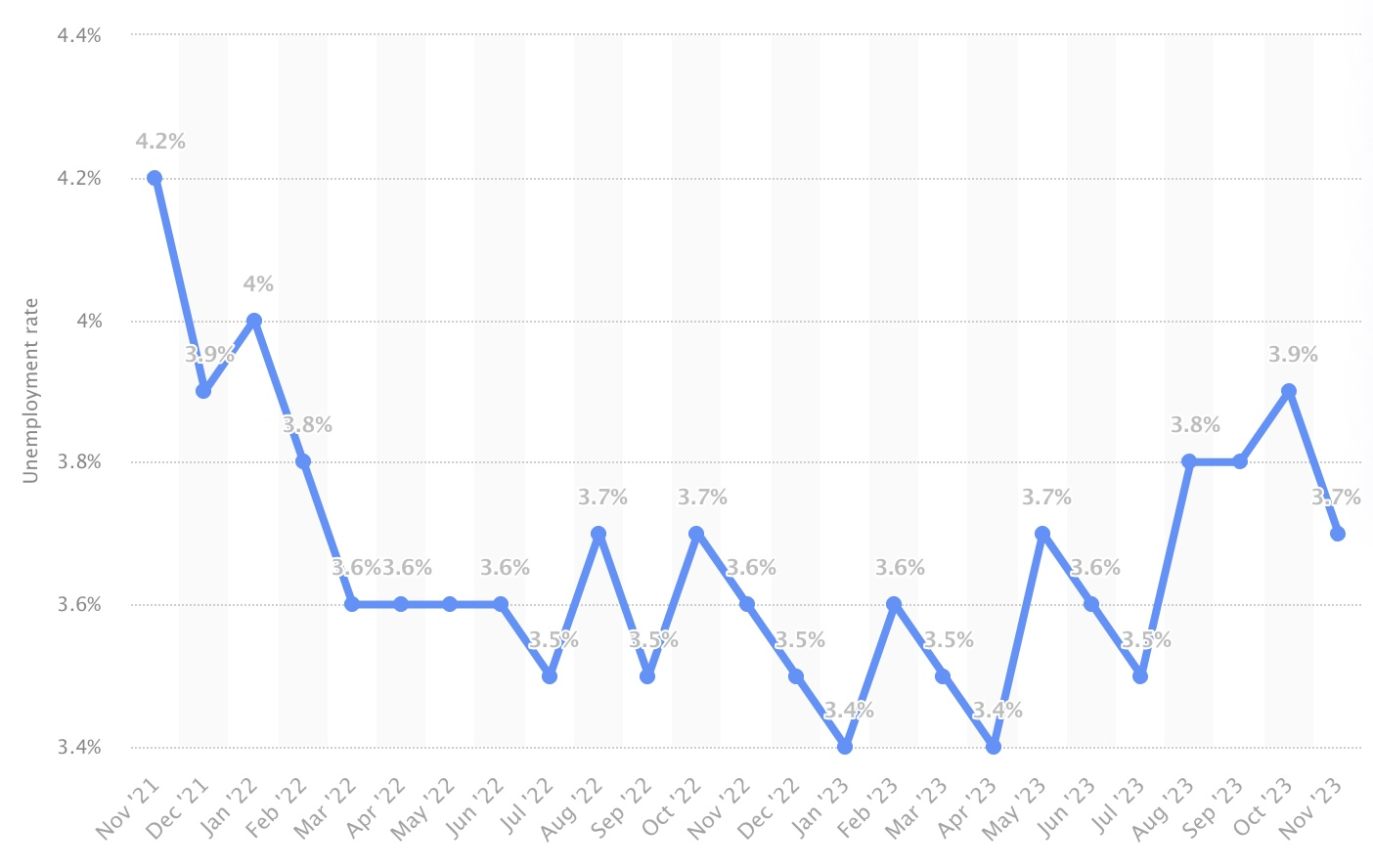

While the Fed has achieved the latter objective, maintaining historically low unemployment levels (from 3.9% in October to 3.7% in November), the tight job market contributes to inflation in services, comprising 42% of the overall U.S. CPI index. Goods inflation may be receding, but services prices continue to climb due to increasing wages, and this trend is expected to persist. Contrary to Chairman Jerome Powell’s suggestion that a slowdown is necessary to curb inflation, personal spending rose by 2.1% to $18.86 trillion in November, indicating a lack of evidence for an economic slowdown.

Structural economic shifts further complicate the inflationary outlook. A shift away from globalisation towards protectionism, evident in the surge of mentions of reshoring, nearshoring, and onshoring during company earnings calls (with an average increase of 216% per year since the beginning of 2022), is accompanied by a higher cost for domestically produced goods. Increased capital costs resulting from interest rate hikes hinder innovation, potentially slowing down productivity gains from artificial intelligence. Additionally, a demographic shift with a decline in middle-income households from 61% to 50%, an increase in the lower-income segment from 25% to 29%, and a rise in upper-income households (14% to 21%) contributes to sustained demand, particularly in the housing market.

The Bureau of Labor Statistics (BLS) documented another consecutive monthly rise in prices within the shelter category, extending an impressive 43-month upward trend. While real-time U.S. CPI data indicates a 0.68% decline in November, there is a discrepancy with research findings suggesting persistent high demand and limited supply. This situation is likely to prolong the housing affordability crisis, adding to the persistence of inflation as we move into 2024. Notably, prices in this category have already shown signs of an upward trajectory in the past two weeks.

While oil prices experienced a decline in November, factors such as the conflict in Gaza and planned OPEC+ production cuts may lead to a resurgence, impacting the transportation sector and contributing to inflation. These factors collectively suggest a forthcoming uptick in inflation in December, prompting the FOMC to face the possibility of another rate hike in early 2024. Despite recent dovish signals, Chairman Powell’s commitment to a 2% inflation target may result in a change of stance. Hence, it is premature for markets to celebrate; the possibility of another rate hike looms on the horizon.

{kind=link}