Despite encountering setbacks and failures, central bank digital currencies (CBDCs) are still being actively promoted by global policymakers. In November, key figures from the International Monetary Fund (IMF), Bretton Woods Committee, and Bank for International Settlements (BIS) urged governments to persist in the development of CBDCs. However, rather than investing further resources in what seems to be a flawed concept, policymakers should reconsider and focus on more essential reforms that can contribute to a more liberated financial system.

The November CBDC campaign commenced with IMF Managing Director Kristalina Georgieva emphasising the need to accelerate CBDC development. Bill Dudley, Chair of the Bretton Woods Committee, not only advocated for the United States to adopt CBDCs but also called for the BIS to establish an international CBDC standard. Additionally, BIS Innovation Hub Head Cecilia Skingsley suggested that CBDCs should not be dismissed as a “solution in search of a problem.”

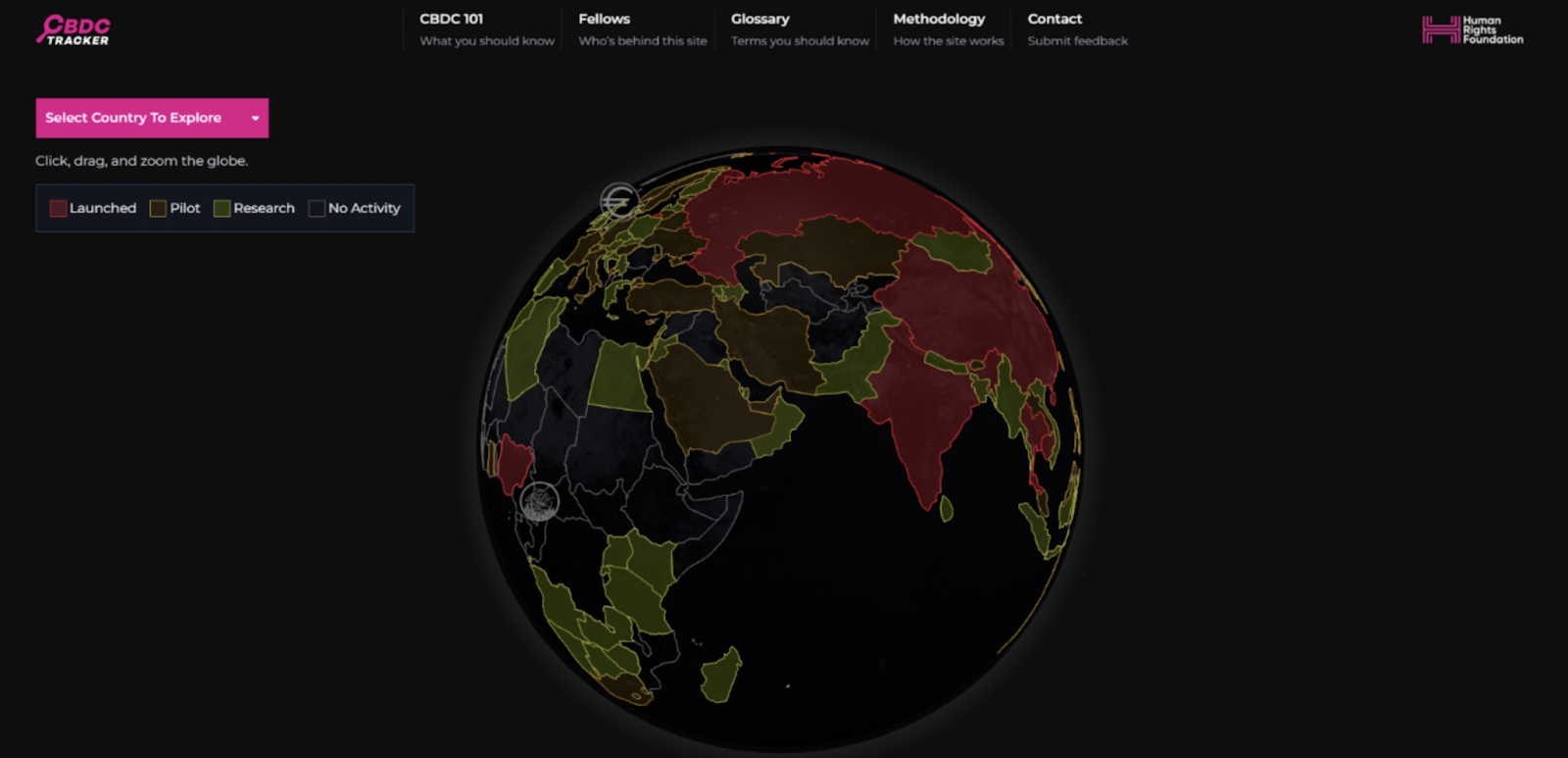

These calls are perplexing considering the current landscape. According to the Human Rights Foundation’s CBDC Tracker, nine countries and the Eastern Caribbean Currency Union’s eight islands have launched CBDCs, 38 countries and Hong Kong have CBDC pilot programs, and 68 countries and 2 currency unions are researching CBDCs. However, none of these projects have proven to be successful.

Examples such as The Bahamas, China, and Jamaica showcase struggles in CBDC adoption, despite incentive programs and giveaways. In China, even after substantial cash giveaways, usage remained low and highly inactive. Some governments, like Thailand, faced delays in CBDC plans due to financial uncertainties and legal concerns, while others, like Nigeria, experienced severe consequences, including protests and riots.

The overall CBDC experience appears to range from government waste to potential government control. Despite these practical failures and associated risks, international organisations like the IMF, Bretton Woods Committee, and BIS continue to advocate for CBDC development.

In light of these failures and potential risks, both the U.S. government and governments globally should reconsider launching CBDCs. The costs outweigh the benefits, and policymakers should not fall prey to the sunk-cost fallacy by allowing prior investments to dictate future decisions.

Instead of pursuing CBDCs, policymakers could focus on reforming the financial system to make it more accessible and open. Various policy reform ideas are available, such as enhancing financial privacy protections and establishing oversight of federal regulators. For instance, reining in financial surveillance, which cost U.S. financial institutions an estimated $46 billion in compliance with reporting requirements in 2022, could lead to a more efficient and cost-effective financial system.

Importantly, reforming financial privacy does not necessitate a complete overhaul of the existing monetary system.

{kind=link}