In October, Bitcoin witnessed a robust 26.5% surge in its price, with key indicators such as BTC futures premium and Grayscale Bitcoin Trust (GBTC) discount hitting one-year highs. However, the bullish scenario is nuanced, influenced by the aftermath of the FTX-Alameda Research collapse recovery and the recent uptick in U.S. Federal Reserve interest rates.

Despite these positive indicators, Bitcoin’s current value remains approximately 50% below its all-time high of $69,900 in November 2021, a notable contrast to gold, which is trading just 4.3% below its March 2022 level. This discrepancy underscores that Bitcoin’s role as an alternative hedge is still in its early stages despite a year-to-date gain of 108%.

To decipher whether the improvements in Bitcoin futures premium, open interest, and GBTC fund premium signify a return to normalcy or the initial signs of institutional interest, investors must assess the broader macroeconomic environment.

The U.S. Treasury’s announced plans to auction $1.6 trillion in debt over the next six months, focusing on shorter-term debt, has raised concerns. Billionaire Stanley Druckenmiller criticised this move and praised Bitcoin as an alternative store of value amid the unprecedented increase in the debt rate by the world’s largest economy.

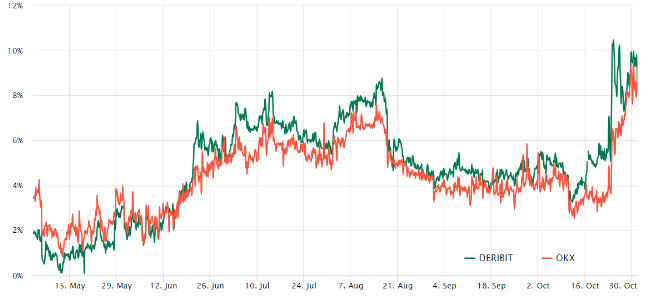

The surge in Bitcoin futures open interest, reaching $15.6 billion, reflects institutional demand driven by inflationary risks. The Chicago Mercantile Exchange (CME) has become the second-largest Bitcoin derivatives trading venue, with $3.5 billion notional of BTC futures. The Bitcoin futures premium, measuring the difference between two-month contracts and the spot price, has hit its highest level over a year, indicating heightened demand for leveraged BTC long positions.

Grayscale’s GBTC fund discount has narrowed from a 20.7% deficit on Sept. 30 to 14.9%, signalling anticipation of a higher likelihood of a spot Bitcoin exchange-traded fund (ETF) approval in the U.S.

However, caution is warranted, especially regarding exchange-provided numbers and unregulated derivatives contracts. The U.S. interest rate rise to 5.25% and increased exchange risks post-FTX suggest a less bullish outlook for the 8.6% Bitcoin futures premium. Nonetheless, in the broader context, this premium is not excessively high, and approval for a spot Bitcoin ETF is estimated at 95%, according to Bloomberg analysts.

Despite positive data, the cryptocurrency market faces general risks, as emphasised by U.S. Senator Cynthia Lummis’s call for action against Binance and Tether. The potential approval of a spot Bitcoin ETF could lead to sell pressure from GBTC holders, allowing them to exit positions after years of restrictions imposed by Grayscale. In essence, the positive data and Bitcoin’s performance reflect a return to the mean rather than exuberant optimism.

{kind=link}