A look at how decentralised applications deliver real and tangible value to investors and market participants in the form of revenue generation and distribution.

Valuing crypto assets

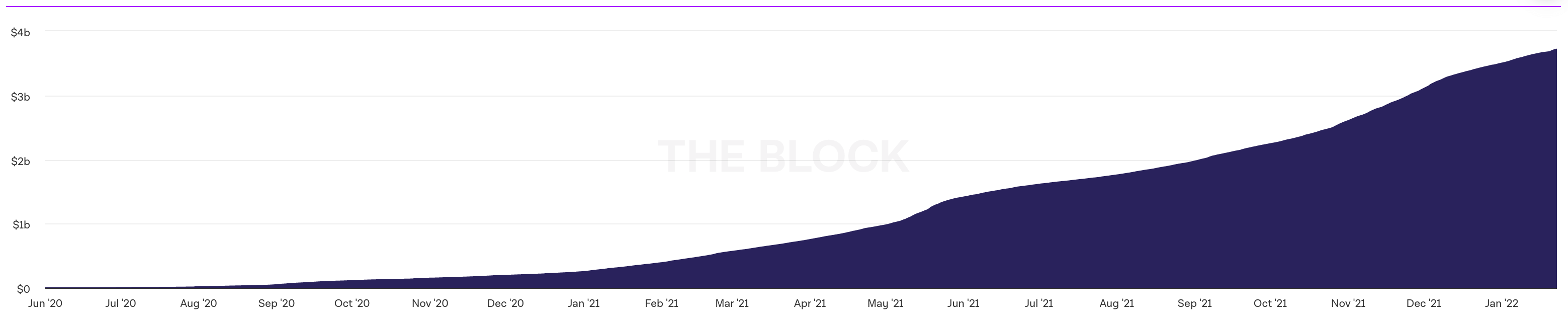

With the broader crypto market experiencing a prolonged bull run throughout 2021, many digital assets have seen their valuations explode, which has led some observers to conclude that crypto is in a bubble. A large part of this reasoning stems from the fact that in many cases crypto valuations are largely based on anticipated future value rather than from real revenue being generated today. However, while this view is certainly not without merit, there are a number of protocols and applications that are already generating real income. According to research from The Block, DeFi protocols on Ethereum had generated over $3 billion USD (or over $4b AUD) by the end of 2021.

Cumulative DeFi Revenue

Source: The Block

Analysing DeFi protocol profitability

Before we dive into the data, we need to define a few key terms. dApps (decentralised applications) are apps that are built to run on blockchains, typically making them immutable, transparent and trustless. DeFi (decentralised finance – if you’re new here and aren’t familiar with DeFi then check out this explainer) is the first and largest dApp sector, and comprises a further three general categories – DEXs (or decentralised exchanges), borrowing & lending protocols and asset management platforms. Whilst TVL (total value locked) dominated the discussion of protocol valuation in the early days of DeFi and remains the metric used by comparison tools such as DeFi Llama, the ease with which TVL can move in search of new and better farming incentives has led investors to increasingly focus on revenue instead, similar to the method of valuation used for a regular company.

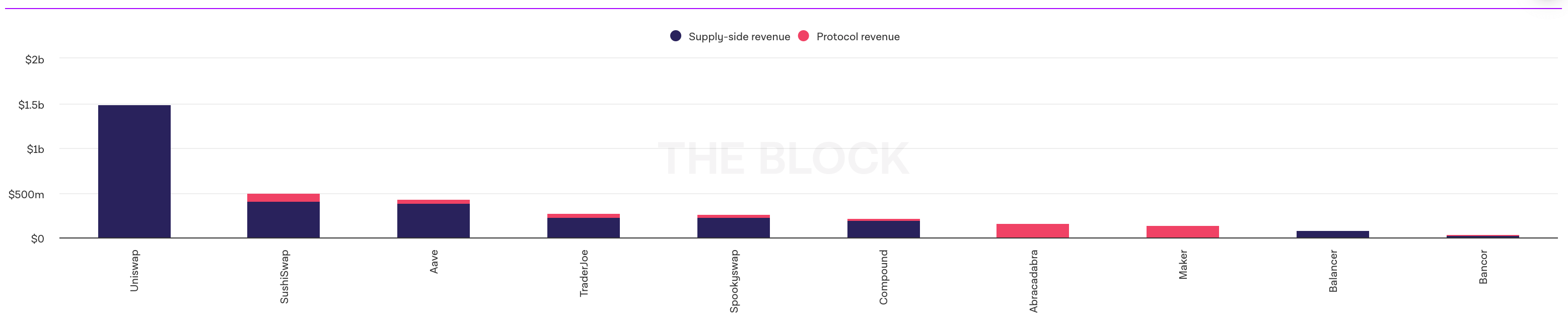

This leads us to a key question – what actually constitutes revenue when we are talking about decentralised applications? This question is more complicated than it appears at first glance due to some of the characteristics that make DeFi decentralised. DeFi protocols and indeed decentralised applications more generally have three different possible channels for revenue distribution: returning value to token holders; to the protocol treasury; or to users of the protocol such as liquidity providers, lenders and borrowers. These first two distribution streams can be grouped together as protocol revenue or ‘earnings’ in TradFi parlance, while the latter is known as supply side revenue and has been pivotal in attracting the liquidity necessary to make decentralised finance work. As we will see, including value returned to users of the protocol makes a massive difference to the stats, with Uniswap going from number one DeFi protocol by total revenue to not appearing at all when ranked by protocol revenue only, as all of the fees generated at present are distributed to liquidity providers (LPs).

Top DeFi protocols by annualised protocol revenue

Source: The Block

Now that we have established what we mean by DeFi protocols and revenue, let’s see what the data from The Block shows for the top DeFi protocols on Ethereum (their publicly available data is only pulled from Ethereum and so excludes other chains that are popular with DeFi enthusiasts). Looking at annualised revenue based on a 30 day sample, it’s clear that Uniswap is the runaway leader with over $1.5B USD (over $2B AUD) in revenue. As noted previously, 100% of this revenue is supply-side revenue, in this case distributed wholly to providers of Uniswap liquidity. DEXs go on to comprise eight of the top eleven protocols for which data is given, with SushiSwap taking second position in the DEX category and third place overall with $369M USD ($512M AUD). Coming in second behind Uniswap is lending protocol Aave with $719M USD ($998M AUD), while Compound is the second placed lending platform and fourth overall with $254MUSD ($353M AUD). Coming in fifth is Maker, the issuer of the DAI stable coin, which has annualised revenue of $150M USD ($208M AUD).

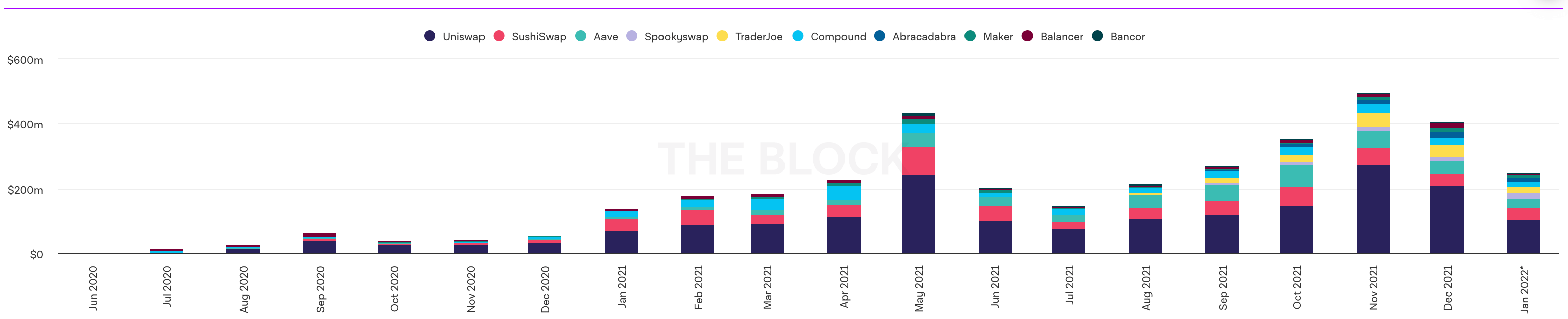

Monthly DeFi revenue by protocol

Source: The Block

If we look at monthly revenue by protocol the picture remains much the same, with Uniswap occupying the top position in every month of 2021, typically accounting for around half of total revenue. In May, the highest grossing month for DeFi in 2021, Uniswap generated $246M USD of a total $466M USD ($341M of $647M AUD). While Sushi and Compound battled it out for second spot in the first part of the year, Aave overtook them to occupy the number two seat in five of the six months in the second half of the year. From this chart we can also see that, while revenue fell sharply following the market crash at the end of May, it recovered quite quickly with the period from September to December seeing the highest monthly revenues outside of the peak of the May boom.

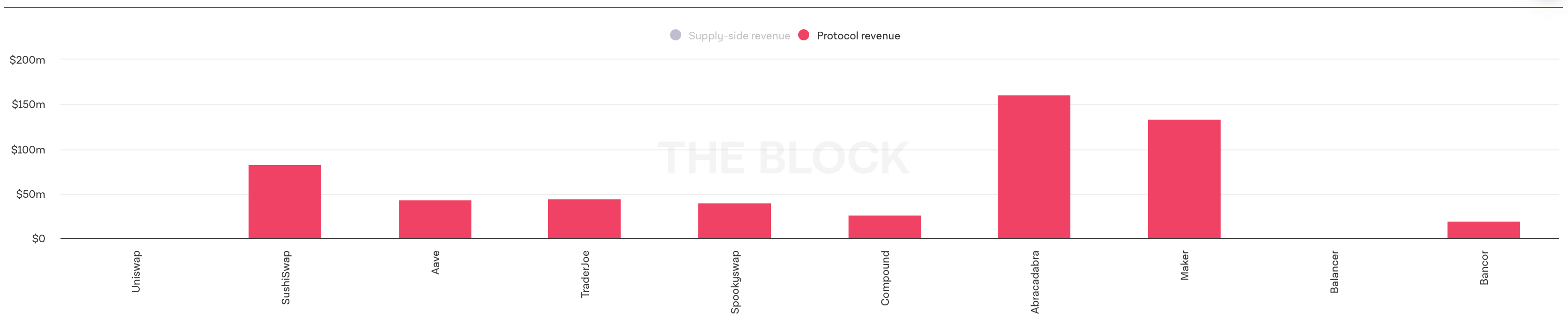

What happens if we exclude supply side revenue?

Source: The Block

The revenue picture looks quite different if we only count value that is captured by the protocol and its token holders and exclude the share of generated revenue that is distributed to LPs and users of the platform. This approach paints a more realistic picture of value capture as understood in mainstream finance, e.g. earnings per share, and has also been pushed by notable figures in the world of crypto such as Sam Bankman Fried. Using the same annualised revenue data from The Block but filtering out supply side revenue, the Maker protocol comes out on top with $150M ($208M AUD), more than double second-placed Sushi with $62M USD ($86M AUD). DEXs fare considerably worse when using this valuation metric, with Uniswap not appearing at all and the top DEX position occupied by Curve with a fairly paltry $15M USD ($21M AUD) of revenue, a state of affairs explained by the fact that most DEXs have chosen to employ all or most of their revenue to attract and deepen liquidity.

Beyond DeFi

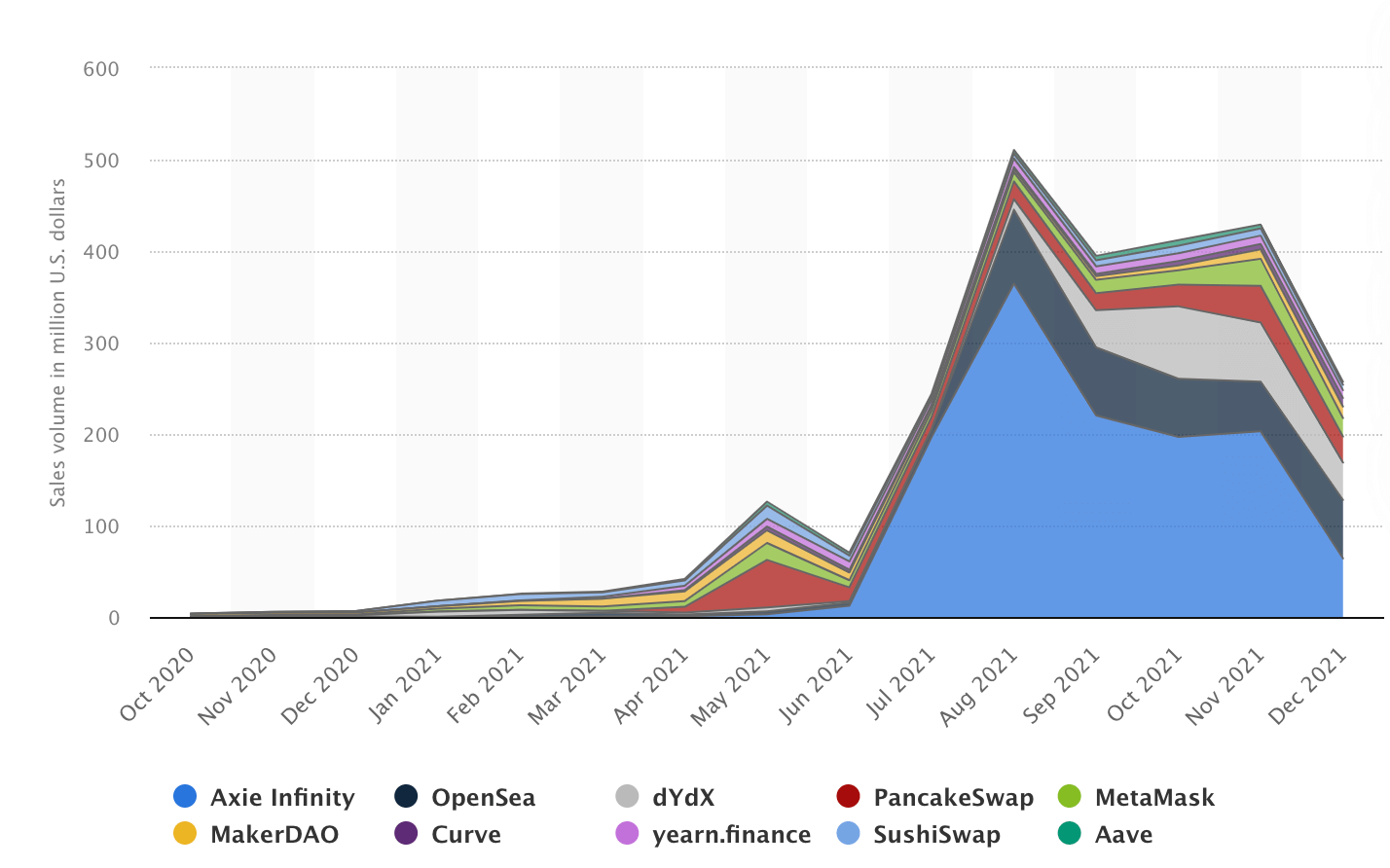

So far we’ve focused on DeFi protocols, but if you kept even half an eye on crypto in 2021 then you will know that the hot areas of growth have been NFTs and crypto gaming, especially play to earn games. So how do dApps in these emergent sectors stack up when compared to their DeFi cousins? This chart from Statista shows the earnings generated by a number of popular dApps, although it excludes supply side revenue and only includes revenue captured by protocols.

Source: Statista

From this data we see popular play to earn game Axie infinity absolutely crushing it in the second half of the year, far surpassing any other dApp for which data is provided and notching up a whopping $364M USD ($505M AUD) at its peak in August 2021, a figure which far out performs the best month enjoyed by Uniswap ($246M USD, $341M AUD) even when supply side revenue is included in the figure for the latter. While Axie’s revenue tailed off somewhat towards the end of the year, it still managed an impressive $64M USD ($89M AUD) in December, just about holding on to top spot on the Statista chart. The second placed dApp in December was OpenSea, representing the other breakout category of 2021 – NFTs. The popular NFT marketplace stormed into second place in August when it generated $81M USD ($112M AUD), more than ten times the revenue it had generated the previous month, and held onto second or third spot through the remaining months of the year.

Non-Ethereum DeFi

The other notable entrants on the Statista chart are DYDX and Pancake Swap, two DEXs that are respectively running on a Starkware layer 2 and Binance Smart Chain and therefore do not show up on the charts from The Block. DYDX finished the year strongly, coming in second behind Axie in October and November, while Pancake Swap had topped the Statista revenue charts in May and June before being toppled by the Axie juggernaut. The second half of 2021 also saw large amounts of capital flow into the Polygon and Avalanche ecosystems, and just last week the Osmosis DEX on Cosmos passed $1M USD in TVL. So, while Ethereum dApps have dominated the revenue narrative up to now, it is possible that the charts for 2022 will tell a different story.

Conclusions

2021 was a record-breaking year in just about every crypto metric you could measure, and dApp revenue was no exception. While debate will continue to rage about how best to capture and portray revenue in a decentralised world, it is important to remember that any sort of revenue generation shows that people are willing to pay for the services that are being offered in DeFi and beyond. As the sector grows and the components of the decentralised finance universe begins to solidify, protocols and their communities can use the decentralised governance processes that are already being put in place to decide how best to distribute revenue so that all stakeholders can benefit from this growth.

{kind=link}